04/10/2026 by Christine Morris

Fuel, Freight, and the Strait of Hormuz Supply Chain Crisis

The Strait of Hormuz closure and the supply chain disruption we’re currently seeing from it – sure feels like we’ve seen something like this before, and it did not resolve quickly.

Remember the Suez Canal? Back in 2021, it became blocked for several days but took months for supply chains to fully recover. The COVID pandemic followed a similar pattern – a sudden shock to global supply chains, exposing just how fragile and interconnected they really are.

That’s the reality of today’s supply chains. Things can break quickly but then often take much longer to stabilize. Even short-lived disruptions can create long recovery cycles in freight.

The current Iran War is shaping up to be another example in supply chain disruption history, except with a different kind of impact. This isn’t just about delayed shipments or port congestion. It’s a multi-layer event that’s affecting fuel markets, manufacturing inputs, and freight demand simultaneously.

In this article, we’ll break down what’s happening in the Strait of Hormuz, why it matters, how it’s impacting supply chains now, and what logistics leaders should be doing to stay ahead and stay resilient.

Iran War and Its Connection to the Strait of Hormuz

The current disruption traces back to the escalation of the Iran War on February 28, 2026, when U.S. and Israeli forces initiated strikes on Iran, prompting retaliation across the region and sharply restricted access to the Strait of Hormuz. This took place after years of rising tension with Iran and previous attempts to negotiate were unsuccessful.

Even ahead of the war initiation, Iran’s Islamic Revolutionary Corps (IRGC) had seized several foreign oil tankers and threatened violence in the Strait of Hormuz.

As of today, there is sustained disruption. Iranian attacks have targeted oil infrastructure in the region, including vessels in the Strait. There have also been several underwater mines employed in the Strait, noted by American intelligence assessments.

And while there are currently no physical blockades preventing ships from traveling through the Strait of Hormuz, there have been threats along with drone and missile attacks that are preventing tankers from going through.

Since the outbreak of the war, there has been a drop of 95% of vessel traffic through the Strait of Hormuz, falling from a daily average of 130 ships per day down to fewer than 100 over the last several weeks.

While Iran has since indicated that “non-hostile” vessels may transit with coordination, uncertainty remains high, which alone is enough to shape behavior in global shipping.

Why the Strait of Hormuz is So Important to Supply Chains

The Strait of Hormuz isn’t just another shipping lanes. It’s one of the most critical chokepoints in global supply chains because:

- Roughly 20% of global petroleum consumption moves through it

- Around 20% of LNG exports pass through it

- Nearly 1/3 of global fertilizer trade relies on this route

Any disruption to the Strait impacts the global pricing of fuel almost immediately. And it’s not just Iranian oil at stake here. The Strait of Hormuz is a key export route for major energy producers in Saudi Arabia, Iraq, Kuwait, Qatar, and UAE.

There are very few alternative lane options that exist to export oil if the Strait is impacted as it’s one of the only routes capable of handling the world’s largest crude carriers at scale.

That’s what makes this different from events like the Suez Canal blockage. Suez primarily impacted containerized goods, affecting certain markets. But Hormuz impacts energy and energy affects everything.

How It’s Affecting Supply Chains

Fuel

The most immediate and visible impact of the Iran War is fuel. Consumers saw it first at the pump. Carriers are now seeing it through rising operating costs. Shippers see it in the form of fuel surcharges and rate adjustments.

“Fuel prices are often one of the earliest and most impactful variables, including both ocean and drayage shipping rates,” said Chad Schilleman, Vice President of Drayage Services at Trinity.

While fuel is the first domino to fall, it’s not the last. Higher fuel costs ripple outward into consumer spending and reduced demand. Over time, that demand pressure will feed right back into the freight markets.

Ocean Freight

So far, the impact on ocean freight has been more measured than expected. Most carriers have already rerouted shipments to avoid the Strait of Hormuz. As a result, import flows have remained relatively stable, although transit times are increasing and costs are rising. Overall, networks are still functioning.

At this stage, this is not a port shutdown or capacity collapse scenario – think more rerouting and added cost pressure.

Domestic Freight

The more significant shift from the Iran War may hit domestically, especially if it continues.

“If the war with Iran is prolonged, it will create a freight need because of the increased demand for defense production. Most of what will be needed can be sourced domestically, if not from a nearshore perspective,” said Greg Massey, Senior Vice President of Agent Development at Trinity.

Recently, the U.S. Pentagon has requested additional funding for defense spending related to the Iran War. If that goes through, there will indeed be a ramp up in the manufacturing and movement of related raw materials, components, and finished goods. This could create a potential upside in pressure on domestic freight demand, particularly in flatbed, specialized freight, and industrial supply chains.

Industry-Level Pressure: Sectors Seeing the Most Disruption

The effects of the Iran War and the disruption in the Strait of Hormuz are not confined to transportation. They are pushing directly into the core of global production. Industries that rely heavily on energy and petrochemical inputs are feeling the pressure first, and in many cases, most acutely.

Automotive

Production depends on a wide range of energy-intensive materials, from coatings and plastics to battery components and semiconductors. At the same time, the Gulf region plays a dual role as both a key shipping route and a major end market for vehicles, especially premium autos.

Fertilizer & Agrochemicals

Agriculture is also under strain, driven largely by the surge in fertilizer prices. Fertilizer prices have surged from $400 to $700 per metric ton since the Iran War began, placing pressure on farmers already operating on tight margins.

Fertilizer production is closely tied to natural gas and petrochemical inputs, so any disruption in energy flows quickly translates into higher agricultural costs. It will impact agriculture cycles, crop production, and overall food pricing, with a downstream effect on food supply chains. There are strong possibilities supply chains may see shortages and increased costs, with early warnings of food security already emerging in the market.

Packaging & Materials

Compared to other materials, plastics (petrochemical based) and aluminum (energy-intensive) are both seeing cost increases. As raw material prices rise, manufacturers are forced to make difficult decisions to either absorb the cost, pass it on, or reduce production.

What ties these industries together is that they are foundational. They all sit upstream of countless other supply chains, meaning disruption here doesn’t stay contained. It cascades outward, impacting everything from consumer goods to industrial manufacturing.

Why This Supply Chain Disruption Will Outlast the Conflict

Even if tension in the Strait of Hormuz eases, the supply chain disruption won’t resolve overnight. That’s because the real challenge isn’t just the event itself, but the imbalance it creates in freight markets.

When shipping patterns need to shift, equipment doesn’t end up where it’s needed. Containers accumulate in some regions while becoming scarce in others. Ports experience congestion unevenly, with some recovering quickly while others remain backed up.

At the same time, contract pricing struggles to keep pace with rapidly changing market conditions, leaving a lag between real costs and agreed upon rates.

Carriers adjust their networks through blank sailings and service changes, but those adjustments take time to stabilize. Meanwhile, inventory flows become misaligned, with goods arriving too early, too late, or in the wrong place entirely.

This is why recovering in freight markets often takes months, not weeks. Stability only returns once balance is restored, and that process is inherently gradual.

Where Disruption Compounds: First-Mile and Drayage

While much of the attention is often placed on ocean transit and long-haul transportation, disruption tends to compound most quickly at the beginning of the supply chain.

Ports become immediate pressure points, especially when volumes shift unevenly or vessels arrive outside of expected schedules. From there, even small delays in drayage can trigger a chain reaction.

A missed pickup or delayed container can impact warehouse operations, delay inventory availability, and ultimately disrupt production schedules.

This is where minor issues escalate into broader operational challenges. Without strong visibility and flexibility at the first mile, it becomes significantly harder to recover downstream.

Freight Market Outlook: Mixed Signals Ahead

The current freight environment is defined by a mix of stability and volatility, depending on where you look.

Short-Term

Import flows have remained relatively stable, largely because ocean carriers have already adapted by rerouting shipments. However, that stability is being offset by rising costs, driven primarily by fuel.

Mid-Term

Looking further out, the picture is more complex. If the Iran War continues, increased defense spending and industrial production could drive new freight demand, particularly in domestic markets. At the same time, regional imbalances are likely to emerge as supply chains adjust unevenly.

Long-Term

Over the long term, one outcome appears increasingly likely: a higher baseline cost structure across transportation modes. Contracts will be repriced, and what was once considered a temporary spike may become part of the new normal.

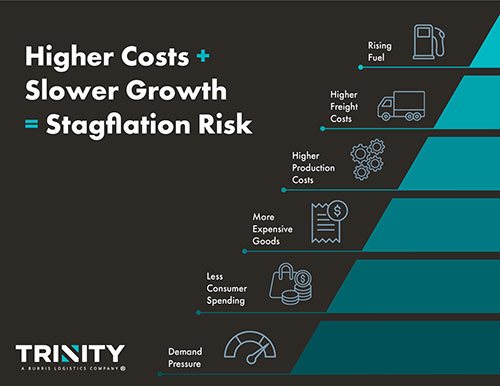

Beyond Freight: Inflation and Stagflation Risk

The impact of the disruption extends beyond logistics into the broader economy. Those higher costs feed directly into production, increasing the price of goods. At the same time, consumers facing higher everyday expenses tend to pull back on spending, putting pressure on demand.

This combination of rising costs paired with slowing growth is what creates the risk of stagflation. It’s a challenging environment not just for supply chains, but for the economy as a whole.

What Logistics Leaders Should Be Watching

In a situation like this, staying informed is critical. However, not all signals carry equal weight, so here are the ones you should be watching.

Strait Activity

Activity in the Strait of Hormuz, including vessel movement and transit patterns, offers a real-time view of risk levels.

Oil & Diesel Price Trends

Oil and diesel price trends provide early insight into cost pressures that will ripple across supply chains.

Carrier Behavior

Rerouting decisions, service adjustments, and capacity shifts can indicate how the market is responding to ongoing disruption.

Regional Congestion Shifts & War Risk Insurance Costs

These patterns and changes can help paint a clearer picture of whether conditions are stabilizing or escalating.

Altogether, these indicators can provide the context needed to make informed decisions during this uncertain environment.

How Shippers Can Strengthen Their Strategy

In today’s market, resilience comes down to preparation and adaptability.

Build Flexibility into Routing & Mode Selection

Shippers that rely too heavily on a single lane, port, or mode are more exposed when disruption occurs. Building flexibility into these strategies will allow for faster adjustments when conditions change.

Reassess Fuel in Budgets & Contracts

With the current impact, fuel can no longer be treated as a stable cost input. Budgeting and contract strategies need to account for ongoing volatility.

Increase First-Mile Visibility & Drayage

Visibility is important here because the small disruptions here can quickly escalate to long-term breakdowns. Understanding where freight is, and where it might get delayed, gives teams the ability to act before issues compound.

Evaluate Inventory Strategy

For critical materials, consider maintaining a buffer of stock to help absorb short-term shocks and prevent production interruptions.

Strengthen Logistics Relationships

Strong relationships across the supply chain matter more than ever in uncertain conditions. Communication and collaboration often outweigh price as the most valuable assets during this time.

Disruption is Today’s Baseline. Resilience is Your Competitive Edge.

If there’s one consistent pattern in global supply chains today, it’s that disruption is no longer the exception – it’s the baseline. And these disruptions rarely resolve as quickly as the headlines fade.

The situation in the Strait of Hormuz makes that clear. Even without a full closure, the ripple effects are already moving through fuel markets, industrial production, and freight networks. Those effects will continue to unfold in the weeks and months ahead.

While in this kind of environment, just having access to capacity isn’t enough.

The companies that stay ahead during this event are doing more than waiting around for things to stabilize. They’re the ones actively monitoring the signals, adjusting their strategies, and making informed decisions before disruption fully materializes in their network.

Often, these companies have access to what’s most critical during disruption – the right partner.

At Trinity Logistics, we don’t just arrange the movement of your freight. We help customers understand what’s happening in the market, what it means for their business, and what to do next.

With real-time market visibility and more than 45 years of experience navigating disruption, we help you stay proactive instead of reactive.

Because supply chain resilience isn’t about avoiding disruption. It’s about being prepared for it, adapting to it, and continuing to move forward while your competition is still trying to catch up.

GET A QUOTE & GET AHEAD OF WHAT'S COMING NEXT